For years, I have enjoyed reading academic papers by Cliff Asness and the team at AQR Capital. A paper by one of AQR’s principals, Andrea Frazzini, entitled “Buffett’s Alpha” as a formative one for me in conceiving of the unique way of measuring and managing leverage in a portfolio I laid out in my 2014 book, The Intelligent Option Investor.

I had always associated AQR with quantitative factor investing, value / momentum overlays, and “risk parity” strategies, but a few years ago, a friend passed along an AQR paper about implementing a covered call strategy entitled Covered Call Strategies: One Fact and Eight Myths.

To me the most interesting idea of the paper was that the authors (Israelov and Nielsen) decomposed the returns of a covered call strategy into two factors: one factor which gives an investor access to earning the market risk premium and another which gives access to the “volatility premium.”

The most accessible part of the paper for most investors is the “one fact, eight myths” piece. I’ve listed these below along with my brief comments. You’ll see that I disagree with the premise of a few of the myths, but that is mainly because of a difference in conceptual framework. AQR has a strong bias for a belief in market efficiency (Asness was a student of Eugene Fama’s at the University of Chicago), which assumes that the present price of the stock is its true intrinsic value. This is a notion that I completely reject (and have good evidence for doing so), so I’m bound not to see eye-to-eye with AQR’s folks on everything.

This is the original AQR paper. It is good, though a little technical in parts. To make it a bit more accessible, I’ve added my own commentary below.

Fact

- Covered calls provide long equity and short volatility exposure: Yes! This is the wonkish point I mentioned above. The short volatility exposure is what we are trying to maximize when affecting this strategy and is the reason I recommend always selling options ATM. Implied volatility is always maximized ATM, so by the age-old investing dictum of “Buy low, Sell high,” you should sell a commodity (in this case, implied volatility) at the highest price you can.

Myths

- Risk exposure can be expressed in a payoff diagram: I totally agree with the authors that those hockey stick diagrams are only valid at one instance in time and don’t give an accurate idea of the risks involved in any option strategy. For that, I much prefer the diagrams I introduced in my book!

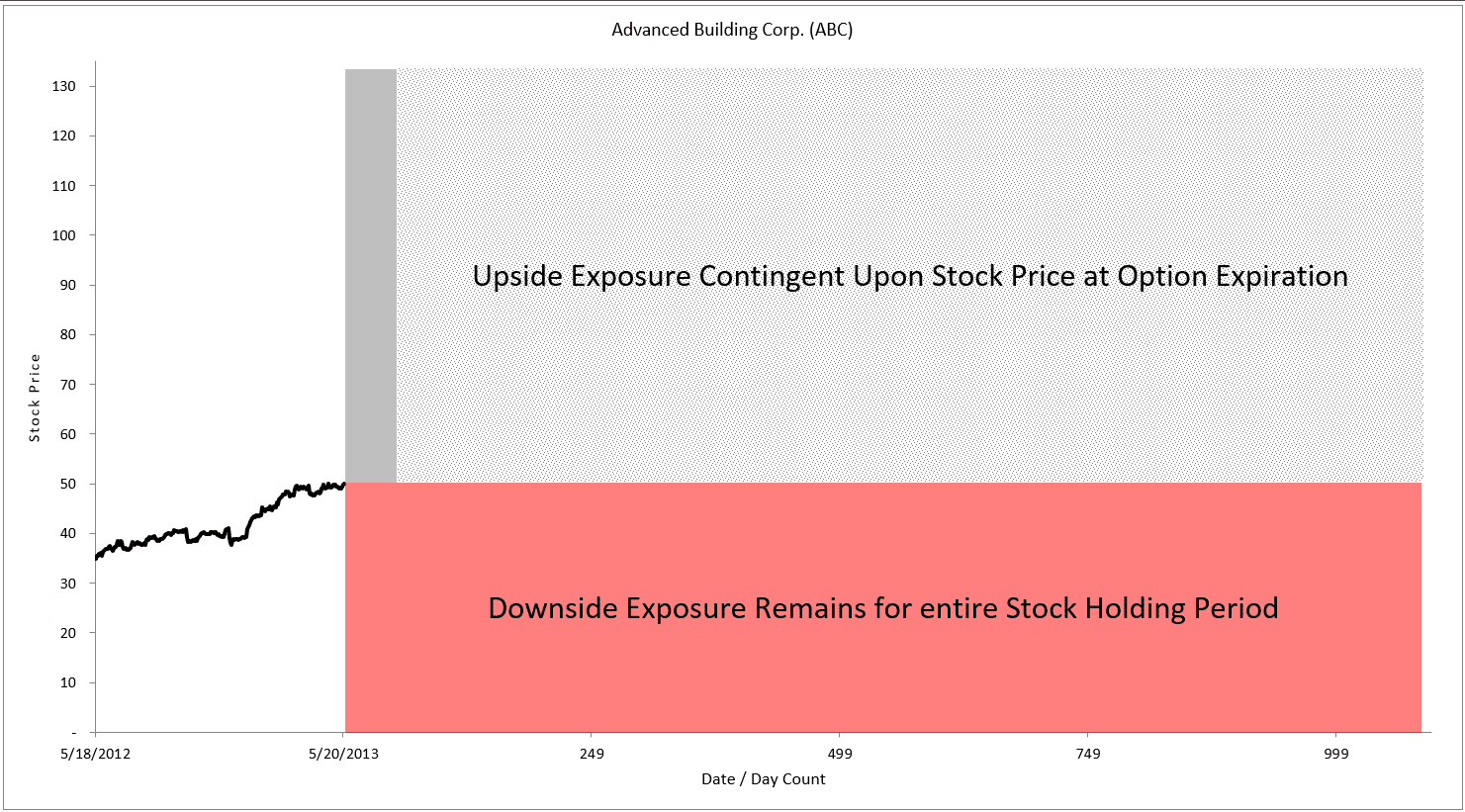

- Covered calls provide downside protection: I totally agree that this is one of the most ridiculous myths about covered calls and can’t believe how many people think they get downside protection from this strategy. There have been many people who have written me emails asking how they could “repair” their position after selling covered calls at a strike price 100% or 200% higher than the present price of the stock. An option premium provides a cushion–usually a thin one–if the price of the underlying shares fall; it does not provide a safety net!

- Covered calls generate income: I laughed when I read the authors’ take on the frequent use of “generate income” as a reason to sell options. The authors are right — one doesn’t generate income if one ends up holding the stock at option expiration. Instead, if at expiration, one holds the stock, one has access to the stock’s upside potential at something I call in my book its “Effective Buy Price” (EBP). As a singer I like once poignantly opined, “…a man technically hasn’t flown till he lands.” Covered call sales generate revenues; one never knows what the income will be until the contract expires!

- Covered calls on high-volatility stocks and / or shorter-dated options provide higher yield: Here is one where AQR’s market efficiency bias makes me quibble. The authors point out that selling a covered call on a high volatility stock is riskier, so the risk-adjusted return is lower. From my perspective as a value-oriented investor, volatility does not equal risk. I would say that covered calls written on a high volatility stock don’t generate better yields if you don’t know how to estimate the value of a stock or if you overestimate its value. The point about shorter-dated options is one that I talk about with regards to the dangers of annualization of returns, which I will turn to in another blog post.

- Time decay of written options works in your favor: Again, this is a myth only as long as you believe that markets are efficient, but I do take the authors’ general point. Every day a short option closes OTM, one can usually feel satisfied about having a tiny unrealized profit on the transaction, as long as the implied volatility has not increased a lot that day. If you count an “unrealized profit” as something working in your favor then time decay does, of course, work in an option seller’s favor. The only time one knows for certain that the transaction has ended in their favor is at expiration, and in this sense, the AQR team is correct.

- Covered calls are appropriate if you have a neutral or moderately bullish view: I totally agree with the authors here. The authors point out that the view that a covered call seller should have is one about the volatility, not the directionality of the stock. Selling covered calls on stocks without regard for what you’re getting paid for volatility is at best an inefficient way to go about the strategy. At worst, it can be fatal, as the super-geniuses in a division of AIG learned in 2009 when they bankrupted the entire company (and nearly wiped out the global financial system) by selling a type of option called a “credit default swap” at far, far too low of an implied volatility.

- Covered calls pay you for doing what you were going to do anyway: I totally agree with the authors when they point out “An option is a contractual obligation, not a plan.” Many people (and even some sophisticated organizations for which I have consulted or worked) talk about selling covered calls as a means of “taking profit.” I can’t stand it when people talk about taking profit using covered calls! Covered calls expose the seller to downside risk in exchange for a fixed fee related to the implied volatility of the option sold.

- Covered calls allow you to buy a stock at a discounted price: I kind-of agree with the authors here. The authors talk about a person who would sell an OTM put to buy a stock if it falls. That is, in my opinion, a silly strategy. However, if you have a good idea of the value of a stock and sell a put to get some contingent exposure at a lower effective buy price, I’m all for it!